U.S.–China Trade Tensions and Global Supply Chains: A New Economic Battleground

U.S.–China Trade Tensions and Global Supply Chains: A New Economic Battleground

The latest escalation in U.S.–China trade tensions highlights a growing struggle that extends far beyond traditional tariffs and import taxes. Today, the competition between the world’s two largest economies centers on critical minerals, rare earth elements, semiconductors, artificial intelligence, electric vehicles, military technology, renewable energy systems, and advanced manufacturing capabilities. Analysts increasingly describe this rivalry as a battle for technological leadership and control of the industries that will shape the global economy for decades to come. In recent days, China announced new export controls affecting several American companies involved in rare earth mining, processing, and advanced industrial supply chains. Among the companies reportedly affected are MP Materials and USA Rare Earth, both considered important players in Washington’s effort to reduce dependence on Chinese-controlled supply networks. The restrictions limit access to certain Chinese products and technologies that have both civilian and military applications. The move represents another chapter in an ongoing cycle of economic retaliation between Washington and Beijing. Over the past several years, the United States has imposed restrictions on Chinese technology firms, limited exports of advanced semiconductor equipment, tightened investment rules, and expanded sanctions on companies linked to China’s military-industrial sector. China has responded with its own export controls, investment restrictions, and efforts to strengthen domestic industries while reducing reliance on Western technology.

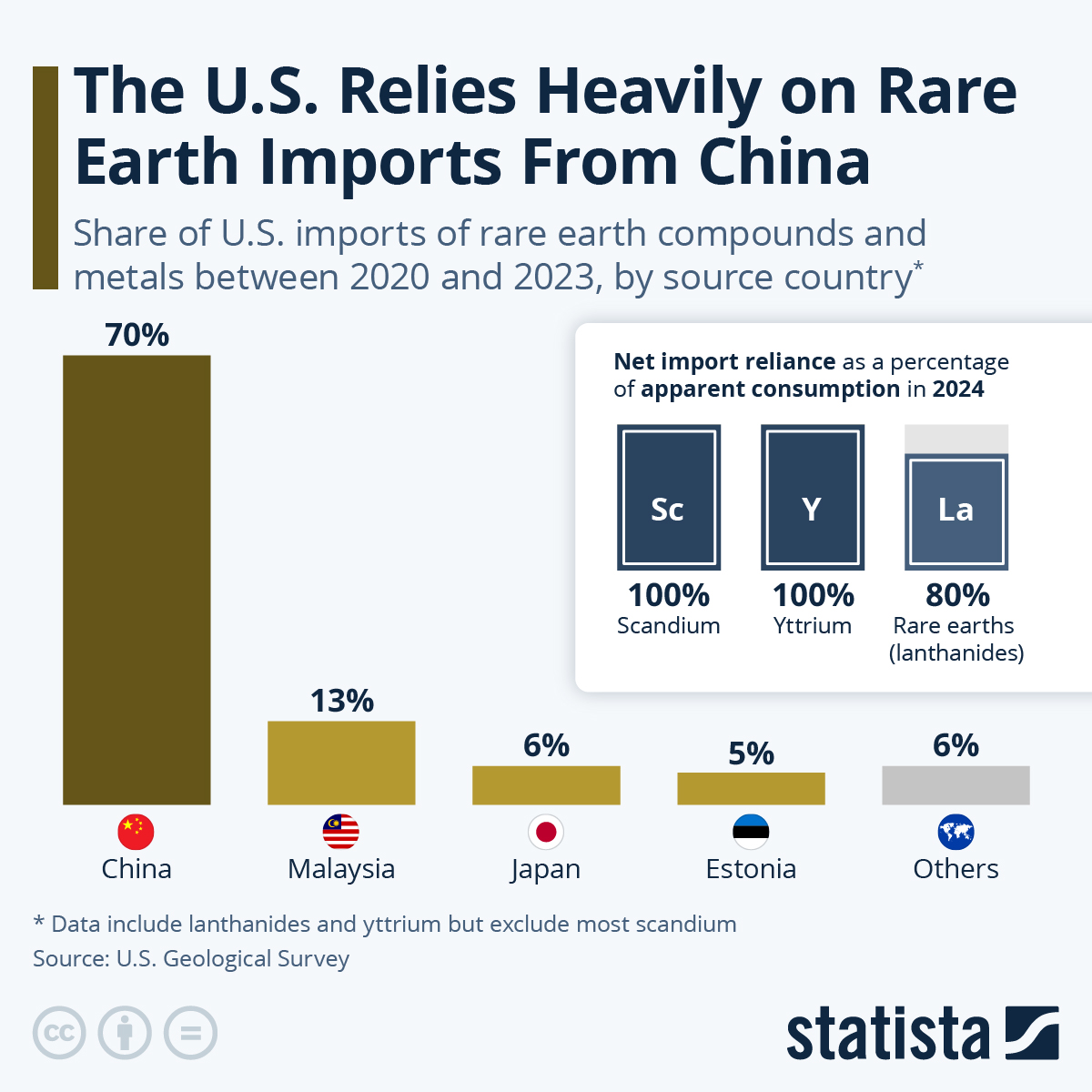

At the center of the current dispute are rare earth minerals, a group of strategically important materials used in countless modern technologies. Despite their name, rare earths are not necessarily scarce in the Earth’s crust. However, mining, refining, and processing them require specialized facilities and expertise. China currently dominates much of the global rare earth supply chain, particularly in processing and magnet production.

These materials are essential for manufacturing electric vehicle motors, wind turbines, smartphones, laptops, advanced medical equipment, military aircraft, guided missiles, drones, robotics systems, satellites, and semiconductor manufacturing equipment. Because they are difficult to replace in many applications, disruptions in supply can have far-reaching economic and national security consequences.

For American manufacturers, China’s export restrictions could create significant challenges. Companies may face rising production costs, longer delivery times, inventory shortages, and increased uncertainty when planning future investments. Industries that rely heavily on advanced electronics, renewable energy technology, aerospace systems, and defense equipment may be particularly vulnerable if supply disruptions become prolonged.

Supply chain experts warn that the issue extends beyond mining. Even when rare earth minerals are extracted in countries such as the United States, Australia, Canada, or various African nations, many still must be shipped to China for refining and processing before they can be used in manufacturing. This means that China maintains influence over a critical portion of the supply chain, even when the raw materials originate elsewhere.

The semiconductor industry remains another major source of friction. The United States has implemented restrictions designed to limit China’s access to the most advanced computer chips and chip-making equipment. American officials argue that these measures are necessary to prevent sensitive technologies from strengthening China’s military capabilities. Chinese officials, however, view the restrictions as an attempt to slow the country’s technological development and economic growth.

Artificial intelligence has also become a key battlefield. Advanced AI systems require enormous computing power and specialized semiconductor chips. As both nations race to develop next-generation AI technologies, access to critical hardware has become increasingly important. The competition is influencing investment decisions, research priorities, and industrial policy across both countries.

Electric vehicles represent another area of growing tension. China has invested heavily in EV manufacturing, battery production, and critical mineral processing for more than a decade. As a result, Chinese companies have become major global competitors in the rapidly expanding clean-energy sector. The United States is now investing billions of dollars through industrial policies aimed at strengthening domestic battery manufacturing and reducing dependence on foreign suppliers.

The consequences of these trade disputes extend well beyond government offices and corporate boardrooms. Consumers could eventually experience higher prices for products ranging from smartphones and laptops to electric vehicles and household appliances. Supply disruptions may also affect renewable energy projects, potentially increasing costs for solar panels, wind turbines, and energy storage systems.

National security concerns are driving many of the policy decisions on both sides. U.S. officials argue that dependence on foreign-controlled supply chains for critical technologies creates strategic vulnerabilities. In a potential crisis or conflict, access to essential materials could become restricted, limiting the ability to manufacture military equipment and advanced technologies.

In response, the United States has launched multiple initiatives designed to strengthen domestic supply chains. Federal investments are supporting new mining projects, battery factories, semiconductor manufacturing plants, and rare earth processing facilities. Policymakers hope these investments will create more resilient supply networks and reduce exposure to geopolitical risks.

One significant development is the effort to establish alternative rare earth supply chains outside China. Companies in North America, Europe, and Australia are investing billions of dollars in new mining operations, refining facilities, and magnet manufacturing plants. These projects are intended to create a more diversified global market and reduce dependence on a single supplier.

Competition for critical minerals has also expanded into Africa, Latin America, and other resource-rich regions. The United States, China, and several European nations are increasingly seeking access to deposits of cobalt, lithium, copper, nickel, and other materials needed for batteries, electronics, and defense technologies. These investments are reshaping global economic relationships and influencing diplomatic strategies.

Many economists describe the current trend as a gradual “de-risking” rather than complete economic separation. While businesses continue to operate across borders, companies are increasingly diversifying suppliers, building additional manufacturing facilities, and reducing reliance on any single country. This strategy aims to improve resilience while maintaining access to global markets.

Financial markets are closely monitoring developments because prolonged trade tensions could affect economic growth worldwide. Investors are particularly focused on industries linked to technology, clean energy, defense manufacturing, and industrial automation. Any major disruption to critical supply chains could have ripple effects across global markets.

Despite rising tensions, the United States and China remain deeply interconnected economically. Bilateral trade still totals hundreds of billions of dollars annually, and many multinational corporations rely on both markets for production and sales. This interdependence makes the relationship complex, with competition and cooperation existing simultaneously.

Business leaders increasingly face difficult decisions about where to locate factories, source materials, and invest capital. Many companies are adopting a “China plus one” strategy, maintaining operations in China while expanding manufacturing capacity in countries such as Vietnam, India, Mexico, Indonesia, and Thailand.

Looking ahead, experts expect technology, minerals, artificial intelligence, semiconductors, and clean-energy industries to remain at the center of U.S.–China competition. Future disputes may increasingly focus on access to resources, intellectual property, advanced manufacturing capabilities, and control of strategic supply chains rather than traditional tariff battles.

The broader significance of this rivalry extends beyond economics. It reflects a global struggle over technological leadership, industrial power, and national security in the twenty-first century. The outcome will influence how products are manufactured, where investments flow, and which nations shape the technologies that define the future.

The main takeaway is clear: the U.S.–China trade conflict is no longer simply a dispute about imports and exports. It has evolved into a far-reaching competition over the resources, technologies, and supply chains that will power the world’s future economy. The decisions made today by governments, businesses, and investors could reshape global commerce for decades to come.